The global financial infrastructure is undergoing significant modernization. For decades, international payments have been managed by an established network of correspondent banks, asynchronous clearing processes, and fragmented accounts. Today, this traditional system is adapting to the demands of a real-time, automated global economy. Stablecoins have evolved into a programmable solution to address these requirements, but is the corporate sector ready to adopt them as a foundational financial layer?

1. Strategic Transition: From Digital Asset Trading to Corporate Infrastructure

Stablecoins are blockchain-based digital currencies designed to track the price of a target asset. Whether backed 1:1 by traditional fiat money like the US Dollar or Euro, or governed by decentralized algorithmic mechanisms, their primary function is to combine the programmable nature and fast settlement times of blockchain technology with reliable price stability.

Currently, the application of stablecoins is expanding beyond digital asset trading into institutional execution and global payment processing. Industry data indicates that 23% of financial institutions have utilized stablecoins [EY-Parthenon, 2025], while 90% are either planning to use or are actively testing stablecoin-based payments [Fireblocks, 2025]. Parallel to this adoption, the market capitalization of stablecoins has reached approximately USD 318 billion in 2026 [Worldline, 2026], with projections suggesting it could grow to $3 trillion by 2030, according to U.S. Treasury Secretary Scott Besent [cited in Higginson, 2026]. Thus, stablecoin are already the 17th largest holder of U.S. Treasures [Matsuoka et al., 2025].

Discussions at the World Economic Forum in Davos highlighted this transition, with banking representatives noting tokenization and stablecoins as central focal points for future development [Chepkova, 2026]. The strategic emphasis is shifting toward practical implementation in the wholesale and large-corporate sectors, as seen with institutional stablecoins like EURAU. This momentum is reflected across the payments industry; as Peter De Caluwe, CEO of Thunes, notes, “treating stablecoins as modern rail for value transfer, we can build a financial system not only faster, cheaper but more resilient, inclusive [WEF, 2026].”

Within this global development, Europe is actively establishing frameworks for adoption. Aided by the legal certainty of the MiCA regulation, institutional barriers are decreasing; a recent survey noted that only 18% of European respondents still view regulation as a primary obstacle [Fireblocks, 2025]. With this regulatory foundation in place, corporate integration is advancing: while 8% of European corporates currently utilize stablecoins, 54% of non-users expect to integrate them within the next 6-12 months [EY-Parthenon, 2025].

2. Recent Developments Advancing the Stablecoin Infrastructure

(Source: https://a16zcrypto.com/posts/article/state-of-crypto-report-2025/, retrieved 2026-06-03)

- Stripe is transitioning its infrastructure on-chain to expedite global money transfers, having acquired Bridge and utilizing a custom “Tempo” blockchain to coordinate conventional and blockchain payment rails into a unified system [Sandor, 2026; Gaibov, 2026].

- Visa has enabled USDC settlements to U.S. banks via the Solana blockchain to support high-throughput, low-cost parallel processing [Visa, 2025].

- PayPal has scaled its federally regulated, dollar-backed stablecoin PYUSD, offering it to users and businesses across 70 international markets [PayPal, 2026].

- SWIFT is developing a blockchain-based shared ledger prototype designed to facilitate 24/7 cross-border transactions across 11,500 institutions [SWIFT, 2026].

- Circle is addressing market demands for alternative payment rails, with USDC steadily establishing itself as a base infrastructure for cross-border transactions [Ciobanu, 2025].

- Allunity, a joint venture involving DWS, Flow Traders, and Galaxy Digital, is issuing EURAU, a MiCA-compliant Euro stablecoin tailored for institutional use, enabling corporate treasuries to process instant cross-border payments [Allunity, 2026].

- Swiss Stablecoin AG [2026] is leading a consortium of Swiss banks, including UBS, to engineer a digital Swiss Franc. Currently in a sandbox phase, this stablecoin functions as a programmable settlement asset for the corporate sector.

- Qivalis and the Euro Stablecoin Initiative have formed a joint venture of twelve European banks (including DekaBank, ING, and Unicredit) to establish a MiCA-compliant Euro stablecoin. It targets B2B and institutional applications by combining traditional banking compliance with blockchain technology [Godenrath, 2025].

- Ant Group, the fintech entity behind Alipay, launched Jovay, an Ethereum Layer-2 network for institutional real-world asset tokenization, acting as a compliant bridge between traditional finance and decentralized ecosystems [Adejumo, 2025].

3. What Transaction Data Reveals: B2B Payments Lead Real Stablecoin Usage

(Source: Mc Kinsey & Company: https://www.mckinsey.com/industries/financial-services/our-insights/stablecoins-in-payments-what-the-raw-transaction-numbers-miss, retrieved 2026-06-03)

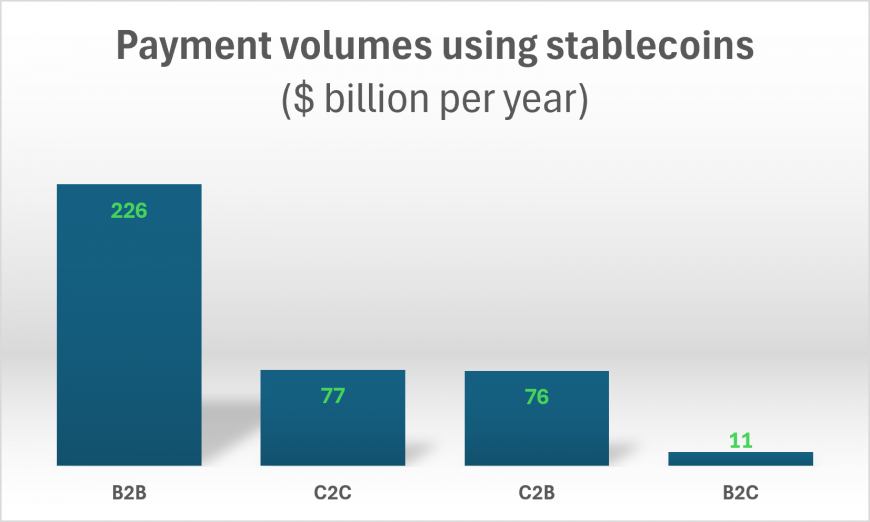

A common misconception is that high on-chain transaction volumes predominantly reflect retail adoption or speculative trading. When examining raw blockchain data, stablecoin transaction volumes are substantial, reaching up to $35 trillion annually [Higginson, 2026]. However, the majority of this figure is driven by trading and decentralized finance liquidity. Isolating these trading applications reveals the actual volume of genuine stablecoin payments, which stands at roughly $390 billion annually [Higginson, 2026].

Retail consumers are not the primary catalyst for stablecoin-based payments. Approximately 60 percent of this genuine payment volume—roughly $226 billion—is directed into the B2B sector for cross-border settlements and improved liquidity management, establishing enterprise usage as a core driver of stablecoin proliferation [Higginson, 2026].

Notably, stablecoin adoption extends well beyond agile fintech startups. Active stablecoin usage is currently highest among large organizations with revenues between $10 billion and $50 billion [EY-Parthenon, 2025]. The return on investment for these corporations is significant: 41% of enterprise stablecoin users report cost savings of at least 10% on B2B cross-border payments [EY-Parthenon, 2025]. To fully realize these savings, companies must strategically manage the fees associated with converting fiat currencies to stablecoins (on-ramping and off-ramping). Nevertheless, industry survey data indicates that cross-border payments and liquidity management remain the primary use cases, driven by corporate mandates to reduce transaction costs, achieve faster settlement times, and secure 24/7 liquidity access [EY-Parthenon, 2025].

Ultimately, the operational advantages of stablecoins translate to large-scale corporate adoption only when built upon a secure, institutional foundation. Alexander Höptner, CEO of AllUnity, emphasizes that global corporations require regulated, Tier-1 infrastructure supported by established financial entities [Bfrr]. With this regulatory and structural foundation in place, corporate treasuries increasingly view stablecoins as a viable, highly efficient alternative to traditional fiat payment rails for managing global cross-border supply chains.

4. Industrial Enterprises Already Utilize Stablecoins for Productive Operations

Industrial enterprises are transitioning from isolated innovation labs to building scalable, concrete infrastructures. The primary economic advantages of stablecoin integration lie in programmable payments, holistic financial management, and the deep automation of supply chains.

In Europe, enterprises are actively developing the infrastructure to facilitate this. SAP, for example, has introduced its Digital Currency Hub, which integrates stablecoin payments directly into corporate ERP systems. This allows companies to bypass the slower correspondent banking system, enabling 24/7 cross-border B2B settlements natively from their accounting software [SAP, 2026].

While public stablecoins have accelerated the shift toward continuous settlement, risk-averse corporate treasuries are equally focused on tokenized bank deposits. According to Citi Institute [2025], these digital representations of insured deposits could support between $100 trillion and $140 trillion in annual transaction flows by 2030. Operating on permissioned ledgers, tokenized deposits combine blockchain automation with the rigorous data privacy and ERP integration required by traditional banking.

Furthermore, stablecoin infrastructure is optimizing the global movement of physical goods, extending deep into traditional heavy-industry supply chains. As Eric Barbier, CEO of the payment gateway Triple-A, points out: “Global trade corridors move billions daily—and now they’re doing it faster with stablecoins. Adoption is being driven by traditional B2B players like ship brokers and steel traders, not just crypto or tech firms. The infrastructure is in place, and the value is clear [Fireblocks, 2025].”

5. From Strategy to Execution: Blueprints for Corporate Stablecoin Applications

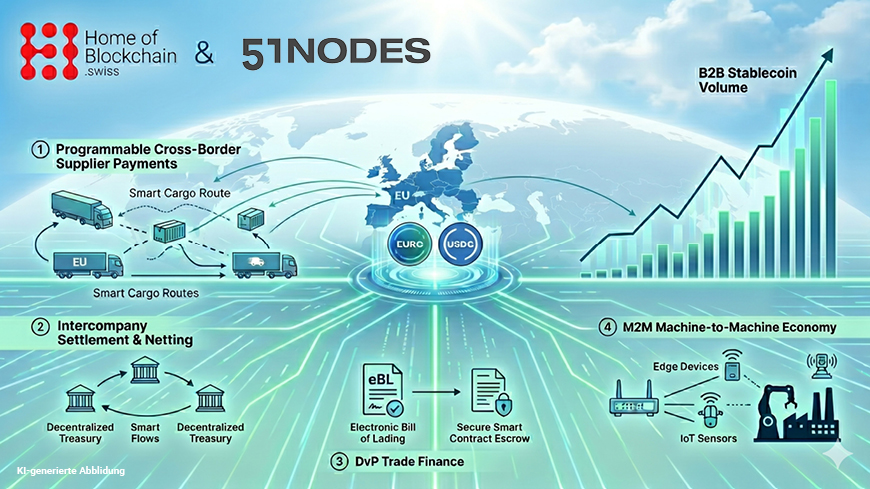

The operational value of stablecoins is realized when programmable business logic reduces friction in international trade corridors. Based on 51nodes’ Stablecoin Use Case Matrix, the following are the highly relevant blueprints driving B2B adoption today:

Programmable Cross-Border Supplier Payments

For industries dependent on non-SEPA imports—such as manufacturing and electronics—stablecoins address costly supply chain inefficiencies. The B2B cross-border stablecoin transaction market is estimated at $13.4 billion in 2026, with projections suggesting it could reach $5 trillion globally by 2035 (93% CAGR), with the volume in Germany alone estimated to reach $160 billion [Juniper Research, 2026]. European importers can automate overseas supplier payouts using stablecoins like EURC, triggered by a confirmed three-way match within modern ERP systems, ensuring same-day liquidity and real-time tracking.

Intercompany Settlement and Netting

Multinational corporations often face trapped liquidity in fragmented local bank accounts when settling invoices between global subsidiaries. To optimize this, treasuries can leverage regulated e-Money Tokens for continuous internal clearing. This programmable infrastructure allows companies to bypass fiat conversion costs and slow correspondent banks, enabling treasuries to sweep idle liquidity and settle internal cross-border balances instantly with the help of an in-house banking module or a centralized Treasury Management System (TMS). This use case targets a global landscape where an estimated €1.8 trillion in excess working capital could be optimized [PWC, 2025].

Delivery-vs-Payment in Trade Finance

In commodities trading and maritime shipping, smart contracts serve as programmable escrows, replacing expensive, paper-based bank letters of credit. Transitioning to decentralized delivery-versus-payment (DvP) offers a solution to help close the significant $1.7 trillion gap in global trade financing availability [FT, 2023]. Triggered natively by an electronic bill of lading (eBL) or IoT sensors, this infrastructure can reduce settlement cycles by up to 10 days while minimizing intermediary fees.

The Machine-to-Machine (M2M) Economy

The expansion of the Internet of Things (IoT) and equipment-as-a-service (EaaS) is turning industrial hardware and AI-driven “machine customers” into independent economic actors, with autonomous agents projected to participate in $30 trillion worth of purchases by 2030 [Constantino, 2025]. Within the foundational IoT payment market—valued at $77 billion in 2025 and expanding at a 42% CAGR [Research Nester, 2025]—industrial entities can stream stablecoin micro-payments directly from edge devices. This stablecoin-backed machine-driven commerce facilitates “pay-per-use” settlement that circumvents traditional credit card acquiring fees.

6. Is Your Organization Prepared for the Evolution of Payments?

The technological evolution of global payments is actively progressing. While stablecoins and tokenized bank deposits will not replace the traditional fiat banking system in the near term, they are compelling it to undergo comprehensive upgrades. The scale of this transformation is substantial: financial institutions surveyed by EY-Parthenon [2025] anticipate that by 2030, stablecoins could account for 5% to 10% of all global payments, representing $2.1 trillion to $4.2 trillion in transaction value (covering B2B, P2P, C2B, and B2C).

Measurable efficiency gains—including error-free atomic settlement, programmable escrow, and the reduction of cross-border B2B friction—have become quantifiable parameters for corporate competitiveness. Organizations that strategically evaluate these advancements now are better positioned to maintain their strategic footing in a digitized, automated global economy.

Prepare your organization for the stablecoin transformation:

Further insights into the practical application of stablecoins can be found in the Stablecoin Use Case Matrix by [51nodes]. The matrix outlines a spectrum of enterprise blueprints, offering a broader perspective on how programmable money can be integrated into corporate infrastructure.

Related links:

Citi Institute, 2025, Beyond Stablecoins: Why Bank Tokens Could Boom

EY-Parthenon, 2025, Stablecoins in focus: navigating the new digital financial landscape

Fireblocks, 2025, State of Stablecoins 2025

Higginson, M. et al. (McKinsey) , 2026, Stablecoins in payments: What the raw transaction numbers miss

Matsuoka, D., Hackett, R., Zhang, J., Zinn, S., Lazzarin, E. (a16zcrypto), 2025, State of Crypto 2025: The year crypto went mainstream